SPACEXAI has five data center locations. Three sites for terrestrial data centers and the fourth is distributed AI with Tesla and the fifth is AI data centers in Space.

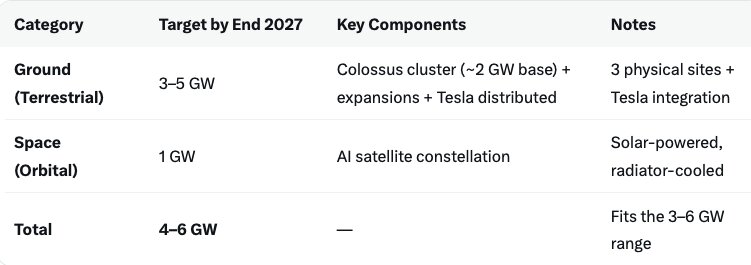

Ground / Terrestrial: 3–5 GWThis is the bulk of the near-to-medium term capacity.Core Colossus Cluster (Memphis, TN + Southaven, MS) — ~2 GW near-term foundation Colossus 1: ~250–500 MW (already operational, ~230k GPUs, leased to Anthropic)

Colossus 2: Targeting ~1–1.3 GW (Blackwell/GB300 ramp)

MACROHARDRR (Building 3): ~500 MW contribution

Combined: ~2 GW total with hundreds of thousands of GPUs (path to 1M GPUs). This matches all recent reporting on the three-site Memphis-area cluster.

Scaling to 3–5 GW by end-2027:

Further expansion of the existing Colossus sites + additional terrestrial capacity + Tesla distributed AI compute

Energy Several 388 MW gas turbines from Korea. Two this year and another 10 over next few years.

$2-3 billion of mobile gas turbines on order for next 3 years.

Colossus 1

Paul R. Lowry Road, Boxtown / Southwest Memphis, Tennessee (old Electrolux factory in Frank C. Pidgeon Industrial Park).

Operational since mid-2024. Scaled rapidly (122 days initial build + 92 days doubling). Now 230,000 NVIDIA GPUs (~150k H100 + ~50k H200 + ~30k GB200). Power draw ~250–400 MW primarily from Memphis Light, Gas and Water (MLGW) grid (TVA-sourced).

Allleased to Anthropic (announced ~May 2026) for inference workloads at ~$1.25 billion per month along with 95000 B200 at Colossus 2.

Mixed-generation architecture made it less optimal for homogeneous frontier training. xAI shifted core Grok training to Colossus 2.

2. Colossus 2 – 550K B200-B300- 1.3 GW

Tulane Road / Whitehaven area, Memphis, Tennessee (1M+ sq ft warehouse acquired March 7, 2025, plus ~100 acres adjacent land). Parts of the broader COLOSSUS II cluster extend operational influence into Southaven, MS.

The Colossus 2 project started March 7th, 2025, when xAI acquired a 1 million sqft warehouse in Memphis, and two adjacent sites totaling 100 acres. By August 22nd, 2025, 119 air-cooled chillers on site, i.e. roughly 200MW of cooling capacity. Enough for roughly 110k GB200 NVL72. And an Elon tweet shows some racks were already installed in July. xAI built in six months what took 15 months for Oracle, Crusoe and OpenAI.

Feb 2026 for the full gigawatt of power to be installed. Chips installations over the next few months.

S-1 said at least 220,000 additional GB300 processors and over 400 additional megawatts of compute power. Does this mean 770,000 GB300?

3. MACROHARDRR (third building)

2400 Stateline Road W, Southaven, Mississippi (DeSoto County. ~48-acre parcel with 810,000 sq ft former GXO Logistics warehouse). Purchased by MZX Tech LLC (xAI affiliate) ~December 23, 2025.

xAI NEWS: An xAI subsidiary acquired the 810,000 sqft GXO warehouse in Southaven, Mississippi, earlier in December from an affiliate of ElmTree Funds, a private equity real estate firm owned by BlackRock.

xAI has built a new road in recent months between Colossus 2 and the GXO… https://t.co/t2jShWfRjp pic.twitter.com/ztGRRbBqJb

— S.E. Robinson, Jr. (@SERobinsonJr) December 30, 2025

Announced by Elon Musk December 30, 2025 (MACROHARDRR pushes our Colossus training compute to ~2 GW).

Conversion to data center began Q1 2026. GPU deployment planned Q2–Q3 2026. Positioned directly across the TN-MS line from Colossus 2 (Tulane Road/Whitehaven area) and adjacent to xAI’s power assets (2875 Stanton Road former Duke Energy site, also acquired by MZX Tech). Part of the ~$20 billion+ regional investment.

Completes the ~2 GW aggregate training cluster. Must be designed liquid-cooling ready for future chips.

Overall cluster layout: Colossus 1 (Memphis TN core, now leased) + Colossus 2 (Memphis TN primary + Southaven MS power tie-in) + MACROHARDRR (Southaven MS warehouse). Power generation heavily concentrated in Southaven, MS (behind-the-meter, avoiding some TN restrictions). The Greater Memphis Chamber’s “no turbines in Memphis” statement holds because turbines sit in Mississippi.

SPACEXAI Power Strategy

(TVA + Dedicated Gas via Solaris JV)TVA Grid (limited but contracted):

Board approved doubling allocation with an additional 150 MW for Memphis-area operations. Contractual commitment: xAI takes no power during grid emergencies/strain. xAI invested ~$35M + $20M in substations and installed 240+ battery units for stability/backup. This supports base load but cannot scale the full cluster alone.Dedicated behind-the-meter gas (core scaling engine): Solaris Energy Infrastructure / Stateline Power JV (verified): Joint venture (Stateline Power LLC, ~50.1% Solaris / 49.9% xAI affiliate). Initial contract upsized from 500 MW to ~900 MW generation capacity; tenor extended to 7 years. xAI represents a massive portion of Solaris’s orderbook (~67% of 1,700 MW = ~1,140 MW weighted).

Current serving xAI: ~400 MW fleet. Additional ~240 MW tied to Colossus 1 site historically.

Solaris secured extra 700 MW of gas turbines (majority deliveries 2026); pro forma operated fleet ~1,400 MW by H1 2027. JV capex already $112M in Q2 2025; total related capex ~$600M. Financing includes up to $550M senior secured term loan.

Mississippi regulators

Approved 41 gas-powered turbines for MZX Tech LLC at the Southaven site (March 2026 construction permit. ongoing operating permit processes and appeals/lawsuits from residents/NAACP/SELC over emissions and prior unpermitted mobile units). These support the permanent plant powering the cluster (including Colossus 2 across the border). Up to 46 temporary/mobile turbines reported operating at peaks.

Caterpillar / Solar Turbines (mobile + efficient units).

Titan-350 models (Solar Turbines, Caterpillar subsidiary; 35–38 MW each, up to ~40% thermal efficiency, mobile/rapid-deploy).

Specific deployments:

7 units at Southaven for Colossus 2 (medium-voltage interconnects). Broader agreements included mixes like 16+16+34 units. Caterpillar/Vertiv collaboration on pre-designed AI data center power + cooling reference architectures (announced 2025). No standalone multi-billion xAI-only Caterpillar contract disclosed separately from the Solaris JV channel.Hybrid model summary: TVA grid for reliable base (with strict curtailment rules) + rapid mobile turbines (Solar Titan) for speed + JV permanent gas fleet (scaling to 900+ MW) for baseload. This enabled the ultra-fast Colossus buildouts but triggered regulatory scrutiny and lawsuits in Southaven.GPU Roadmap — Quarter-by-Quarter + Technical Depth (Verified S-1 Language)S-1 key disclosure (exact): Next phase of expansion at Colossus 2 “will bring online at least 220,000 additional GB300 processors and over 400 additional megawatts of compute power.”Colossus 1: ~220k–230k GPUs (mixed H100/H200/GB200). Fully leased to Anthropic (inference).

Colossus 2: Homogeneous Blackwell. Initial large batch of GB200/GB300 chips ramping (hundreds of thousands targeted). Current live compute building toward higher utilization.

MACROHARDRR: Conversion Q1 2026 → GPU deployment Q2–Q3 2026.

Contributes to aggregate push toward ~1 million total GPUs / ~2 GW.

Blackwell GB300 specifics (next Colossus 2 tranche). ~15 petaFLOPS dense FP4, 288 GB HBM3e, 8 TB/s bandwidth, 1,400 W TDP.

GB300 NVL72 rack 1.1 ExaFLOPS FP4 (1.5× GB200 NVL72 AI performance). Air-coolable but higher density than prior gens.

Rubin (Vera Rubin / R200 platform)

Volume shipments targeted H2 2026.

~50 petaFLOPS FP4 per GPU (vs. 15 for B300/GB300). Pairs with Vera Arm CPU (88 custom “Olympus” cores).

Power: 1,800–2,300 W per GPU; no air-cooled configuration — 100% liquid cooling required.

Retrofitting air-cooled facilities

6–12 months construction + major capex.

MACROHARDRR (and any future phases) must be liquid-cooling ready from the start.

Earliest realistic xAI Rubin deployment: late 2026 or 2027.

20% Rubin allocation

Altimeter Capital (Clark Tang) analysis and related investor commentary (including BG2 pod discussions with Brad Gerstner/Gavin Baker) indicate xAI/SpaceX secured up to ~20% of early Vera Rubin capacity from Nvidia (scarce initial supply). This gives xAI a significant edge for 2026–2027 scaling. Commentary also highlights xAI’s fast build speed enabling first-mover Blackwell advantage (early 2026 models expected from xAI per Jensen Huang notes) and strong infrastructure economics (high IRR on Colossus assets; monetization via leasing generates attractive operating profit per GW vs. peers).

Turbine contracts and orders (precise from SpaceX S-1 IPO filing, May 2026, which discusses xAI as a division/subsidiary post-February 2026 acquisition by SpaceX)

~$2.8 billion total committed for natural gas turbines over the next ~3 years for AI infrastructure.

Specific ~$2 billion purchase agreement (late April 2026) for mobile gas turbines and related equipment from an unnamed vendor (one report notes it as pending at filing time).

Additional agreements (~$805–925 million range across reports) for more turbines through 2029.

Doosan Enerbility (South Korea) large turbines (380 MW-class gas turbines + generators. for permanent plant capacity)

Initial order: 2 turbines (contract ~Oct 2025. supply targeted by end of 2026 or so).

Additional 5 turbines (confirmed by Elon Musk early 2026).

Further Order for 7 more (announced ~March 2026). Deliveries of one per month starting May 2029. Reports indicate total of ~12 turbines under contract with this supplier for the data center project.

Quarter-by-quarter

Through Q4 2025: Colossus 1 scaled/mixed. Colossus 2 warehouse acquired + early cooling/GPU ramp (Blackwell start). MACROHARDRR purchased (Dec).

Q1 2026

MACROHARDRR conversion begins. 41-turbine permit approved (MS). additional TVA power. mobile turbines scaling.

Q2–Q3 2026

Major GPU additions (220k+ GB300 on Colossus 2 + 400+ MW). MACROHARDRR GPUs online. Permanent JV turbines ramping. Rubin prep (liquid cooling).

Q4 2026+

Rubin integration begins (liquid-cooled phases). Aggregate toward 1M GPUs / 2 GW. Full JV fleet maturation (~1.1+ GW turbines by Q2 2027).

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.